Tax Proposal Would Make Getting a PhD in the US Very Expensive (Multiple Updates)

The tax plan introduced by Republicans in the U.S. Congress last week would have drastic effects on graduate education in the United States, according to reports at The Chronicle of Higher Education and Inside Higher Ed.

[UPDATE: The rest of the original post is below, however, as commenters Genevieve and Michael E. Lopez point out (and as I acknowledge in a comment), is based on an error. (Though see the green text below for why, though I was mistaken, the bottom line about the tuition waivers being taxed under the proposal may nonetheless be correct.)

The section of the proposal from which I quoted appears to be about how to calculate one’s income for determining eligibility for an education tax credit (I believe it’s the “Lifetime Learning Credit” in the existing code and the “American Opportunity Tax Credit” in the proposal), and not about determining one’s taxable income.

I apologize for the error.

As I mentioned in the OP, a few readers pointed me towards sources on this, including this piece in The Chronicle of Higher Education, which says, “The plan would also tax the tuition waivers that many graduate students receive when they work as teaching assistants or researchers,” and also this widely shared Twitter thread from a professor at UT Austin, which says “GOP tax bill would tax tuition wavers for grad students.” I thought I should fact-check these claims, and so I searched through to the tax code and the Republican proposal to see what they said about tuition. I found language that appeared to explain these claims, and wrote up the post. This was a mistake: tax law is complicated and can be written in a confusing manner. Though I included disclaimers in my original post, I should have checked with an expert. Lesson learned.

The question remains as to whether there is some other part of the proposal that explains the claims about tuition waivers being taxed. If there is, I did not find it, but I also did not spend much more time today looking. If you find anything relevant, please share it in the comments. Thank you.]

[UPDATE 2: Commenters believe that the relevant bit is “striking subsection (d) of section 117,” listed on p. 96 of the proposal. Here is what 117(d) currently says:

(d) Qualified tuition reduction

Gross income shall not include any qualified tuition reduction.

(A) such employee, or

(B) any person treated as an employee (or whose use is treated as an employee use) under the rules of section 132(h).

Paragraph (1) shall apply with respect to any qualified tuition reduction provided with respect to any highly compensated employee only if such reduction is available on substantially the same terms to each member of a group of employees which is defined under a reasonable classification set up by the employer which does not discriminate in favor of highly compensated employees (within the meaning of section 414(q)). For purposes of this paragraph, the term “highly compensated employee” has the meaning given such term by section 414(q).

In the case of the education of an individual who is a graduate student at an educational organization described in section 170(b)(1)(A)(ii) and who is engaged in teaching or research activities for such organization, paragraph (2) shall be applied as if it did not contain the phrase “(below the graduate level)”.

Gross income does not include any amount received as a qualified scholarship by an individual who is a candidate for a degree at an educational organization described in section 170(b)(1)(A)(ii).

(b) Qualified scholarship

For purposes of this section—

(1) In general

The term “qualified scholarship” means any amount received by an individual as a scholarship or fellowship grant to the extent the individual establishes that, in accordance with the conditions of the grant, such amount was used for qualified tuition and related expenses.

(2) Qualified tuition and related expenses

For purposes of paragraph (1), the term “qualified tuition and related expenses” means—

(A) tuition and fees required for the enrollment or attendance of a student at an educational organization described in section 170(b)(1)(A)(ii), and

(B) fees, books, supplies, and equipment required for courses of instruction at such an educational organization.

The worry, I believe, arises from 117(c), which excludes from the amount of “qualified scholarships” that are not to be counted as taxable income “that portion of any amount received which represents payment for teaching, research, or other services by the student required as a condition for receiving the qualified scholarship or qualified tuition reduction.” However, while stipends seem to fall under “that portion,” it is not clear whether tuition waivers do. For an argument that they do, see this comment by “C”.

Advice from experts welcome.]

The plan has many parts, but of particular interest to academics may be the clause that would require graduate students to pay taxes on the value of the tuition waivers they receive.

In philosophy, as with many other fields, most PhD students do not pay tuition—rather, it is paid, ultimately, by the university itself (in various ways, depending on scholarships, the budgeting structure, etc.). This amount varies from school to school, from around $14,000 per year at public universities like the University of South Carolina or the University of Colorado, Boulder, to around $48,000 at Georgetown University or Princeton University.

In addition to this benefit, most such students also receive a modest stipend, usually in exchange for being a teaching assistant, instructor, or research assistant. Though there are some exceptions, a PhD student’s take home pay is typically small, with students earning just enough to get by.

Currently, graduate students do not pay taxes on the value of the tuition waiver they receive from their universities. That amount counts as “qualified tuition and related expenses” and as such is not treated as part of their taxable income. According to Title 26, Subtitle A, Chapter 1, Subchapter B, Part III, § 117 of the U.S. Code: “(a) Gross income does not include any amount received as a qualified scholarship by an individual who is a candidate for a degree” at most universities, and “(b.1) the term ‘qualified scholarship’ means any amount received by an individual as a scholarship or fellowship grant to the extent the individual establishes that, in accordance with the conditions of the grant, such amount was used for qualified tuition and related expenses.”

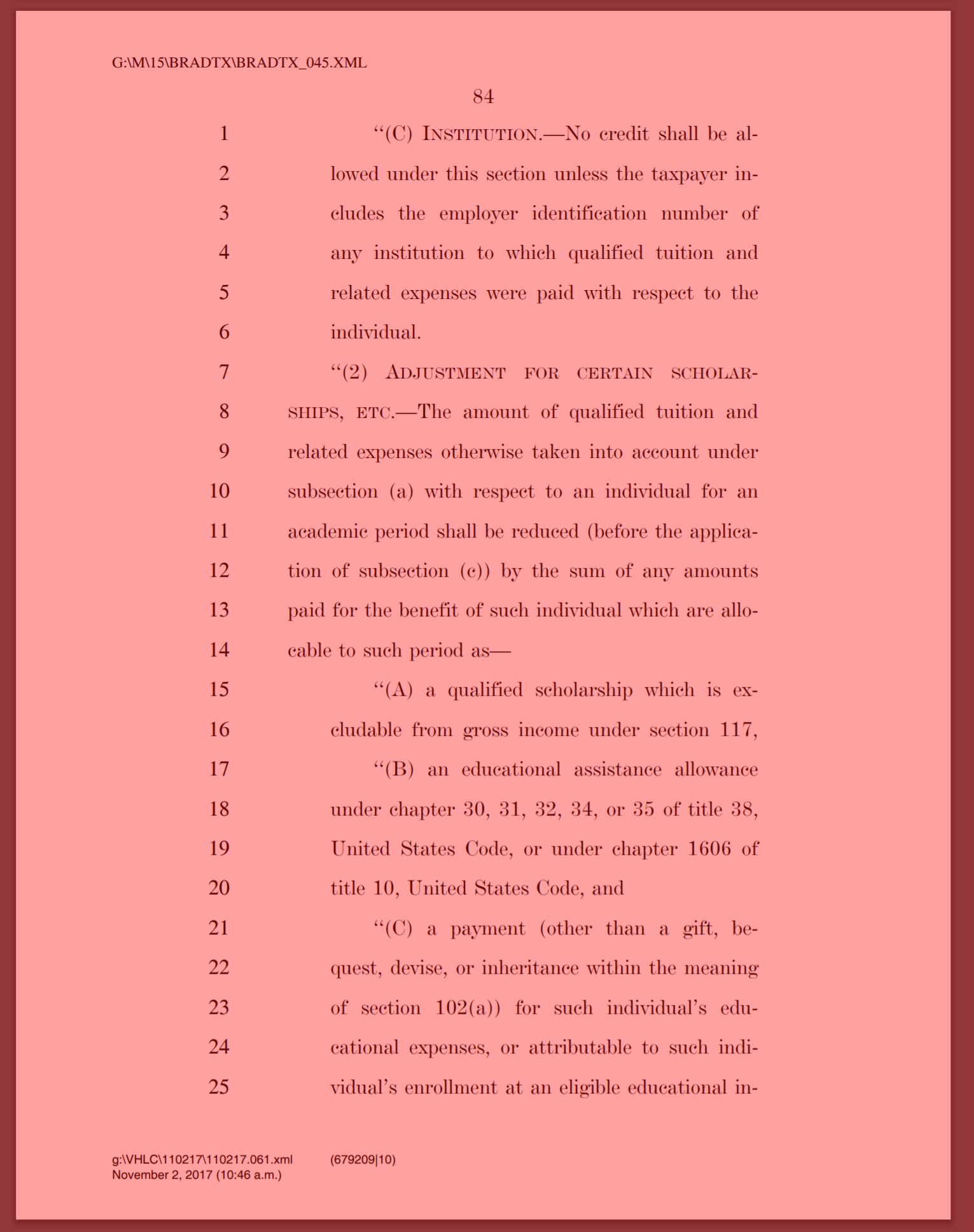

My understanding—please correct me if I’m wrong**, folks—is that the new proposal removes “qualified scholarships” from the “qualified tuition and related expenses” graduate students were previously not taxed on:

The amount of qualified tuition and related expenses otherwise taken into account under subsection (a) with respect to an individual for an academic period shall be reduced (before the application of subsection (c)) by the sum of any amounts paid for the benefit of such individual which are allocable to such period as— ‘‘(A) a qualified scholarship which is excludable from gross income under section 117…

That’s from p.84 of the proposal, under “Subtitle C—Simplification and Reform of Education Incentives”, (sec.25A)(f)(2). (My apologies if this isn’t quite right; I’m not used to reading tax bills.)

If that’s correct, then a graduate student who receives a $20,000 stipend for being a teaching assistant, plus a $40,000 tuition waiver, will have to pay taxes on an income of $60,000.

[* I’m wrong. See the red update above.] [*But nonetheless the tuition waivers may count as taxable income. See the green update, above.]

That leaves aside other credits and deductions, but note that even if the graduate student is receiving benefits that count as “qualified tuition and related expenses” under the new proposal, any tax credits for such expenses are “allowed only for first 5 years of postsecondary education,” with significant reductions in the fifth year, which means it will be unavailable for most graduate students for most of their graduate education (see p. 80 — Sec.25A(d)).

Suggestions about what to do in regards to this proposal are most welcome.

(Thanks to a few readers who suggested posting about this, one of whom recommended this Twitter thread from Claus Wilke (UT Austin) and another who added, “I remember that when the GOP took over congress in 1995 they proposed this and backtracked pretty quickly, but I think academics should pay attention this time.”)

This will put some of us, myself included, in an interesting position: I generally favour higher taxes. I also believe, perhaps less popularly, that the privilege I enjoy studying philosophy at the graduate level saddles with me with responsibilities to give back. One way of doing that–one among others–is to pay more tax.

But I also cannot afford to pay more tax, as I’m barely getting by right now.

The upshot is that for many reasons the US is becoming an undesirable place to live and study. Though it’s been far from horrible, living here for years has been an eye-opener. I look forward to returning home and and building a life there. Too many things are circling the drain in this country at the moment.

Can this be fixed with some different bookkeeping: e.g., just make graduate schools have free tuition (at places/programs that provided waivers)? It seems likely that the whole “charge tuition but then provide a waiver” gambit was for tax purposes anyway, but I don’t know.

Prof. Claus Wilke claims in his Twitter thread, private schools *might* be able to find work arounds like this, but public schools probably won’t. I haven’t seen that claim verified, but it seems plausible.

David Burbach had a short thread in response to this proposal:

“Would cost univs a gigantic amount in sponsored research funding, which in many fields includes the tuition remission for grad assistants”

“I.e., set tuition to $1, and funding from NSF, NIH, corporations, etc declines accordingly since you can’t bill them tuition costs anymore”

“Students never see that money of course, but outside humanities it’s generally not just an accounting fiction”

The David Walsh thread that takes off from is also worth reading, for how this will cut his take-home pay by one third. (Someone later down said that due to other provisions it would be more like one quarter, but still.)

There would also probably be other knock-on effects. For instance, I’m definitely not a legal expert, but if a grad student or family member is getting subsidized insurance through the Affordable Care Act, this seems like it would be likely to price them out of it.

I would suspect in a lot of states the legislatures will have to take action. I can also see the IRS ignoring any pretextual tuition charges for funded students, and insisting that the value of the tuition remission is whatever non-funded graduate students pay.

Most grad students get insurance as part of their student benefits, right? I did. And did everyone I recall chatting to.

I know lots of grad students in the States who *don’t* get health insurance as part of their benefits. I don’t know whether that undermines the “most” claim, but I can at least confirm that many PhD programs don’t include that kind of coverage.

Anyway, the insurance example was only meant as one way in which having your nominal income go from 25K to 60K (or whatever the numbers might be) might affect you even if the university were to raise your stipend enough to compensate for the tax increase. (Which would cost the university a lot of money, in any case.)

My University also doesn’t give us insurance as a benefit. They used to provide a subsity to make it cheaper, but now they don’t even do this.

After reading the bill, I’m inclined to think that what it’s saying is that we can’t put the $60k (which we definitely don’t make) towards a tax credit, but that the scholarship amount won’t count towards our gross income either. So, in essence, we don’t pay taxes for the amount that goes towards tuition, but we also can’t use it as a tax credit. Does that sound right? Maybe that’s just optimistic…

You couldn’t use it as a tax credit before, as far as I know.

The primary means of upward mobility in our society is through education. This tax plan puts a filter on disadvantaged and middle-class graduate students as you can’t live off the stipend and pay taxes on ~60k income! These are the people that are going to allow the US to compete in an increasingly knowledge-based economy. This plan is not only short-sighted but targeting students of modest and even middle-class means. On the flip side, the GOP tax plan is repealing the Estate Taxes to create a new financial aristocracy class aka Old Money.

Get out vote these people out.

the GOP tax plan is repealing the Estate Taxes to create a new financial aristocracy class aka Old Money.

And on that subject, the plan not only repeals the estate tax but keeps the stepped-up basis for capital gains, which would mean gigantic fortunes never get taxed.

Duncan “Atrios” Black explains a bit here, but the idea is this: If Rich Uncle Pennybags acquires $4 million in stock, the value of that appreciates to $5 million, and then he sells it, he pays taxes on the $1 million in capital gains realized.

But if Rich Uncle Pennybags dies and leaves that $5 million to Cousin Pennybags, and Cousin Pennybags sells it right away, Cousin Pennybags doesn’t pay capital gains tax. Cousin Pennybags would only pay estate tax on capital gains over and above the $5 million value the stock had at the moment of inheritance. This is the stepped-up basis; the “basis” from which capital gains gets calculated gets stepped up to the value at the moment of inheritance.

Under current law, what happens is that the $5 million gets taxed as part of Rich Uncle Pennybags’ estate. But repealing the estate tax without removing the stepped-up basis would mean that that $4 million of capital gains never gets taxed at all. Which is something that never happens to the money that you and I make (unless you’re one of the very small number of DN readers who is the heir to a dynastic fortune). Even leaving aside the federal income tax, every cent of it is subject to the payroll tax.

…which goes to International Grad Student’s point above. Yes, I feel that we ought to give back, and the overall level of taxation should be higher. As someone with an above-average income (unlike grad students), I even think there are tax proposals that would increase my tax burden that would be fair. But not a tax bill that increases tax on me, let alone graduate students, in order to ensure that Donald Trump’s family and a tiny number of other rich people can inherit tax-free. That’s not right.

The cynical response to this (which I don’t necessarily endorse) is that Democrats should let Republicans do the dirty work of raising upper-middle-class taxes, and then when they’re in office, reverse the tax cuts for the super-wealthy.

“My understanding—please correct me if I’m wrong, folks—is that the new proposal removes “qualified scholarships” from the “qualified tuition and related expenses” graduate students were previously not taxed on”

You’re wrong. Genevieve is right.

This language is about a tax credit, not about income.

Of course, telling you that you’re wrong — even if you issue a correction or take down this post — is not going to change the fact that your article has been linked on Facebook and has been seen by thousands of people, all of whom think that they are going to be taxed on scholarships because someone couldn’t be bothered to read pages 82-83 before spouting off about page 84.

“because someone couldn’t be bothered to read pages 82-83 before spouting off about page 84.”

No need for that, Michael.

—

I took another look at the text of the proposed changes and the original code. The passage from the proposed changes that I quoted in my original post is indeed from a section that is headed (on p.78) by “(a) IN GENERAL.—Section 25A is amended to read as follows:…”.

Section 25A in the Code is about the Hope and Lifetime Learning Credits.

So I think that Michael and Genevieve are right about the parts of the proposal I quoted. Thanks for the correction.

I will have to update this post.

Is there some other part of the proposal that states or implies that tuition waivers would be taxed under it?

I ask, because, besides me, several others were led to that conclusion, including The Chronicle of Higher Education in the article I linked to in the OP (“The plan would also tax the tuition waivers that many graduate students receive when they work as teaching assistants or researchers”), in Claus Wilke’s Twitter thread, which I referred to in the parenthetical at the bottom of the OP, and by the American Council on Education in this letter (referred to by Inside Higher Ed today).

Check page 97-99 of the tax bill (from a simple search in the PDF). The ACE, etc. ARE CORRECT. They ARE striking section 117(d). They just mention it earlier on page 84, because you can’t get a tax credit from a provision that will no longer exist. Michael is peddling in FAKE NEWS.

https://www.congress.gov/115/bills/hr1/BILLS-115hr1ih.pdf

Perhaps — but one question I had about that is what difference it makes to PhD students to strike 117(d) if 117(a) is left in place?

From what I can parse, reading around the net, scholarships are what are given to undergrads. Graduate student wages are a combination of a qualified tuition waiver and a grant which is treated as wages. Perhaps there is some accounting wizardry that universities can perform to dodge the striking of 117(d), but as things stand now, grad students would be effected (as they are treated as employees in this case). Again, perhaps universities could restructure how they do things (or not. I’m no accountant), but why even risk something so heinous!?

See Example 2, page 8:

http://www.ucop.edu/financial-accounting/_files/taxation/t-182-77.pdf

I’m not a tax lawyer (if anyone involved in this discussion is, please advise), but from a quick reading the big difference to PhD students from striking 117(d) and leaving 117(a) in place comes from 117(c)(1):

“(c) Limitation

(1) In general

Except as provided in paragraph (2), subsections (a) and (d) shall not apply to that portion of any amount received which represents payment for teaching, research, or other services by the student required as a condition for receiving the qualified scholarship or qualified tuition reduction.”

(The House bill would strike “and (d)” from this, since (d) doesn’t exist anymore. Paragraph (2) isn’t really relevant for our purposes. The thing about subsection (d) not applying to this payment seems to be overridden by 117(d)(5) which explicitly deals with teaching and research assistants. A strictly logical reading might mean that section (c) nevertheless excluded graduate and teaching assistants from (d)(5), since that’s part of (d), but I suspect there’s a statutory principle along the lines of “It would be completely ridiculous to exclude the very people that (d)(5) explicitly is supposed to apply to from (d)(5). Again, not a lawyer.)

Again, as a not-tax-lawyer, this seems like it would mean that graduate programs couldn’t give grad students tax-exempt waivers for teaching fellowships or research fellowships. They would have to be straight-up grants. Perhaps this could be finessed by giving scholarships to cover tuition and having the actual pay conditional on teaching/research assistantships, but this seems likely to cause knock-on problems.

Fair credit to Kimberly below fo bringing up the point that repealing 117(d) might leave open the possibility that tuition waivers could be reclassified as scholarships.

Just a speculation (because I’m not a tax lawyer either), but maybe the 117(d) repeal isn’t really aimed at graduate students. It might be aimed more at universities who deduct graduate student waivers as employee benefits. If the goal of this tax plan is to squeeze more taxes out of the university system, then making sure they can’t deduct waivers would be one way. If that’s the case, then there probably isn’t a reason why the university can’t reclassify waivers as scholarships/grants. They haven’t done so because it wasn’t really to their benefit given the tax code.

Just to be clear, is the new bill striking 117(d) itself? From page 99 under (e) CONFORMING AMENDMENTS RELATING TO SECTION 117(d), it seems to only strike reference to 117(d) in the context of 117(c)(1) – as well as 414(n)(3)(C) and 414(t)(2) – but not 117(d) itself. If that’s the case and my reading of 117(c)(1) is right, the current laws state that the part of a qualified scholarship that is payment for teaching/research is NOT exempt from taxable gross income (that’s 117(a)). Likewise, the part of a qualified tuition reduction that is payment for teaching/research is NOT exempt from taxable gross income (that’s 117(d)). The new proposal would be to remove the second limitation. But I think 117(d) would still exist? And moreover, tuition reduction still is not taxable income even if it’s payment for teaching/research.

I could be missing something, though!

Disregard, found the striking of 117(d) on page 97 SEC. 1204 (a) (3).

Yes, tuition waivers would be taxed without 117d. Tuition waivers are DISTINCT FROM “fellowships or scholarships”; they are employment benefits—a form of compensation for labor. In particular, they are a “qualified tuition reduction”.

117d2: ““qualified tuition reduction” means the amount of any reduction in tuition provided to an employee of [a University] for the education (below graduate level) […] of [that employee or their family].”

117d5 exists to fit graduate students employed by their university into the 117d2 definition.

The tuition waiver received by an administrative assistant for their child’s BA is exactly the same as the tuition waiver a graduate student gets while employed as a TA. 117d2 keeps the admin’s tuition waiver off of their gross income, 117d5 keeps it off of the graduate student’s gross income.

Additionally, this tool put out by the IRS treats “tuition waivers” and “scholarships/grants” differently: https://www.irs.gov/help/ita/do-i-include-my-scholarship-fellowship-or-education-grant-as-income-on-my-tax-return

But, how do we know whether a **particular instance** of tuition disappearing from a graduate student’s life is being treated by their university as a fellowship/scholarship (QS/117a) or a tuition waiver (QTR/117d)? We look at the tax forms! YAY! (…)

1: The 1098t forms provided by my university DO NOT include TA/GSI tuition waivers in box 5, “scholarships and grants”. By contrast, regular (non-teaching) fellowships are included under “scholarships and grants” — with the full amount, tuition AND stipend (from which we deduct qualified tuition to get taxable scholarship income). This means they are being handled completely differently, administratively speaking. (Tuition waivers are also, appropriately, not included in our W2s.)

2: For the sake of further clarification. The IRS states: “You must include in gross income: […] Amounts received as payments for teaching, research, or other services required as a condition for receiving the scholarship or fellowship grant.” So, if you got a fellowship (117a) rather than a tuition waiver (117d), it would have to show up *somewhere* on your 1098t (or, I guess, W2). Since it does not, at least at my university, they are regarding our tuition waivers as 117d (which does *not* show up on gross income) rather than 117a.

So, I can’t answer whether a TA’s waiver MUST be taxed with 117d gone, but, retrospectively, I’m pretty certain mine would have been.

Genevieve — yes, the bill strikes all of 117d. The changes to other sections are for the sake of consistency.

Kimberly — Having spoken with tax lawyers in my family, I agree that this is not aimed at graduate students. It’s administrators and faculty getting free, untaxed tuition for their families that are in the crosshairs.

(I really should be grading papers.)

The IRS quote is from this page, btw: https://www.irs.gov/taxtopics/tc400/tc421

(sorry!)

Ah I found it on page 97, thanks! That’s really unfortunate for us students then, despite what the ‘aim’ of the proposal may be.

Naive question: If all of 117(d) is removed, then doesn’t that remove the definition of tuition reduction that includes grad TAs and RAs as receiving one?

ACE writes that the proposed tax plan would repeal “the exclusion from gross income of qualified tuition reductions provided by educational institutions under Code Sec. 117(d).” You should look at the language in 117(d), which is the section that currently keeps tuition waivers tax free. If repealed, then that exception is repealed. More info on 117(d): https://www.irs.gov/pub/irs-wd/201516030.pdf

My question is whether universities could simply reclassify their “waivers” as scholarships. If used for tuition and books rather than living expenses, scholarships are tax exempt. I don’t think that’s changing. Currently, grad tuition waivers fall under 117(d) because we’re considered “employees” receiving the waiver as a benefit in return for services. I assume that means that the uni can deduct those employee benefits from their own taxes, which might be part of the reason we get waivers instead of scholarships. (Of course, universities only consider us employees when it’s convenient for them. Other times, like when we’re trying to unionize, it’s so much more convenient for them to consider us students. But that’s a whole different story.)

Before jumping in, I just want to say that I think this tax bill would be a disaster for lots of reasons, but I think it is important to understand exactly what it would do. In particular, it isn’t clear to me that fee waivers would be taxable under the proposal, and even if they would be, there’s still an easy fix that universities could implement. No doubt, the proposed bill eliminates 107(d), which clearly states that fee waivers are excluded from taxable income. So it certainly looks as though fee waivers would be taxable under the proposal. But 107(a)-(b) also clearly states that scholarships used for stuff like tuition is excluded from taxable income. The question, then, is whether fee waivers fit the IRS definition of a scholarship. It is at least arguable that they do. From the IRS: “A scholarship is generally an amount paid or allowed to a student at an educational institution for the purpose of study.” It seems that a fee waiver is an amount allowed to a student at an educational institution for the purpose of study. So, I’m unconvinced that the bill would actually render tuition waivers taxable. But I would also hate for the future of graduate study in America to depend on a question of tax law interpretation. Luckily, given that 107(a)-(b) is not being eliminated, there’s an easy fix that universities could implement, and it’s the one that Kimberly has already noticed. If universities simply stopped offering tuition waivers and instead offered scholarships that cover tuition, the problem would be solved because even under the proposed bill, scholarships (of certain sorts) remain excluded from taxable income. Kimberly suggests that a problem with this proposed solution could be that universities can deduct benefits they offer to employees from their own taxes, so they wouldn’t want to switch from offering fee waivers to scholarships. I don’t immediately see why scholarships wouldn’t also count as benefits (same worry about this whole thing turning on a matter of tax law interpretation). But surely losing the tax benefit would be worth the cost if the alternative is that no one can afford to go to graduate school. Universities would lose a huge source of their own cheap labor (grad student teachers and TAs), and there would pretty quickly be a shortage of academics (since no one could afford to become one). So I think we should definitely fight the passage of the bill, but we should perhaps be hopeful that, at least with respect to taxing graduate student tuition waivers, it’s not as bad as it looks.

Though Ian, as above, I’d point to 117(c) which specifically states that any compensation consistent on work done would be taxable–currently that seems to be superseded by 117(d)(5) but that’s repealed in the bill. That’d seem to hit most grad programs that attach the tuition waivers to teaching assistantships or research assistantships.

I’m not sure that I see why 117(d)(5) supersedes 117(c). All 117(d)(5) does is specify that in the case of graduate students, we read 117(d)(2) as if it didn’t include the phrase “below the graduate level.” Am I missing something?

I take it that 117(c) is just specifying that any money that graduate students receive for teaching or research that does not go towards things like tuition is included in taxable income. But, as has become a refrain, I’m not a tax lawyer either.

I mean, I don’t know exactly, and it’s not my business to know–but it is the American Council on Education’s business to know, so I think that the best approach would be to take their word for it unless they’re clearly wrong.

There’s also this paper from Edvisors, whoever they may be, which mentions 117(d)(5) as adding an exclusion from income for qualified tuition reductions for graduate students who were teaching or research assistants; which mentions that that exclusion had been removed in the Tax Reform Act of 1986.

There’s also this from 1987 by Sandra McMullan, the Executive Director for Tax Policy and General Counsel of The National Association of Independent Colleges and Universities (which makes her probably the single most experty person there was at the time), talking about the impact of the 1986 Act and how it meant that any portion of a scholarship that was compensation for teaching or research would be taxed. In particular, see note 12; “In 1984, Congress amended former Section 117(d), which authorized tuition remission for

education below the graduate level for dependents of employees, to permit tuition remission for

graduate student teaching and research assistants,” which the main text says was reversed in the 1986 act; apparently this was made necessary by previous IRS rulings. McMullan’s letter makes clear how much chaos this had the potential to cause. The 1988 act seems to have added 117(d)(5) specifically to overturn this… so taking away 117(d)(5) would seem to bring it back.

Soooo… what I’m saying is that neither I nor any of the people on the thread is the best person to ask, and I’d point you to the experts. But if you really want my reading of the text, 117(c) says that anything a student gets for teaching or research, including tuition reductions (“the qualified scholarship or qualified tuition reduction”), doesn’t get excluded from income as specified in section (d). That specifically means what’s excluded is not the portion that doesn’t go to things like tuition, it’s everything that was conditional on your getting the TAship–stipend and tuition reduction. Now (d)(1) says that qualified reductions don’t count as income, (d)(2) says universities can give qualified reductions for undergraduate college tuiton to their employees (and family, which is what section 132(h) does)–and then (d)(5) says that when the employee is a TA or RA they can get a qualified reduction on graduate tuition too. If it weren’t for (d)(5) there’d be no provision that allows any employee to get a qualified tuition reduction for graduate tuition.

As I said a strictly literal reading of (c) might suggest that (d)(5) doesn’t actually apply to compensation that’s done for the TA/RA work, but that would seem to make (d)(5) a total dead letter, so I’d guess it doesn’t apply that way? Again, this is where you want an actual lawyer or expert to look at it. (Michael E. Lopez is a lawyer, I believe, but it seemed like his comment was specifically about the part Justin highlighted, which wasn’t actually the relevant language.)

I looked at this in detail and wrote something up for my fellow grad students. Here is what I understand is the purpose of 117 (d) 5:

117(d) in general gives a waiver for fringe benefits of tuition reduction. This normally applies to staff or family of faculty. If you search the code for “tuition reduction” you find it listed elsewhere among other fringe benefits.

117(b) limits this to undergraduate coursework only. It applies to employees themselves, and to their family (that’s specified in §132 h, which 117(b)2 points to). That means if you had hoped (like I do) on getting your kids free through college wherever you teach, you would now need to pony up the taxes for the tuition you don’t have to pay.

What 117(b)5 did was to extend this to also cover tuition for doing graduate school work, but only if it included teaching and research responsibility. I am assuming this mostly prevents a tax write-off for the tuition waived if your spouse or family goes to med school, law school, or business school as an employee fringe benefit, since those grad schools often don’t have research or teaching requirements. So, the only time a grad student would fall under this section is if somehow the University did not consider the tuition remission a scholarship, but a fringe benefit of being employed as a researcher or teacher.

One possible way I could conceive of this is the following: I know at my MA program some did not have funding. If someone is paying tuition, but takes an opportunity to teach a class as an adjunct at the same university, and the university has a reduced tuition rate for adjunct instructors, then this tuition reduction would now be taxable. I can see this happening, but probably not as a frequent case. Just in case, I did re-check my acceptance to make sure it said “Tuition Scholarship,” so I’m quite confident it falls under 117(a)

Though I would not call myself an expert on tax law, I am a lawyer with some specialized experience litigating the tax code (though not this specific section). As I read it this really will make tuition reductions taxable; as it stands now, the code narrowly carves out tuition reduction from taxable income. The GOP plan will totally remove any advantageous treatment of tuition reduction.

While it’s a little unclear about what constitutes a tuition deduction vs a scholarship, scholarships are not tax-free if they require research or teaching duties (117(c)(1)), removing the vast majority of graduate tuition waivers from eligibility.

Also, if there was any doubt, since this plan is meant to squeeze money out of graduate students, they wouldn’t strike 107(d) if that didn’t help them meet that goal.

I’m definitely not an expert in tax law. Nevertheless, the first order evidence seems relatively clear:

(117(c)(1)) says “Except as provided in paragraph (2), subsections (a) and (d) shall not apply to that portion of any amount received which represents payment for teaching, research, or other services by the student required as a condition for receiving the qualified scholarship or qualified tuition reduction.

This is the clause that makes it the case that we currently already pay taxes on the stipend/salary/scholarship beyond the tuition. In contrast, what is exempt is specified by (117(b)):

(b) Qualified scholarshipFor purposes of this section—

(1) In general

The term “qualified scholarship” means any amount received by an individual as a scholarship or fellowship grant to the extent the individual establishes that, in accordance with the conditions of the grant, such amount was used for qualified tuition and related expenses.

That in turn qualifies what falls under 117(a):

Gross income does not include any amount received as a qualified scholarship

If you search the tax code for “scholarship” and for “tuition reduction” it becomes more clear that “tuition reduction” is only used to refer to the fringe benefits that employees or staff get. What 117(d)5 eliminates is tuition reductions (a.k.a. the fringe benefit of an employee) for grad students doing research. If you have a child that is a grad student at your university, they are doing research, and they are not funded by a scholarship, like other grad students, but by your faculty fringe benefits, then this would make their tuition reduction taxable.

I really don’t see any other way to read this code.

Maybe I should add that my admission letter clearly states that I am receiving a “Tuition Scholarship” and not a “Tuition Reduction.” Insofar as the acceptance letter is a legal document, and what I am to receive is given the name of one thing, and not another thing, named in the tax code, I have absolutely no qualms not claiming my tuition scholarship on my taxes, and if the IRS wants to take me to court over that I don’t see how they would win.

Kolja,

As per your first post: The tuition remission — all of it — is in the vast majority of cases done because of your research and teaching duties. It’s a benefit along with the stipend, because those research and teaching duties are inseparable from what you are required to do as a graduate student. It’s part and parcel of the benefits you receive as a graduate student from doing your duties. A scholarship with no research or teaching requirements is certainly possible; I know some organizations grant no-strings-attached grants that don’t require you to produce anything. But those are going to be in a distinct minority.

As per your second post: What the university says is not particularly relevant to the IRS’s analysis, unfortunately. A lot of the IRS’s enforcement duties revolve around deciding exactly how things like income should be classified under the tax code, and whether the parties paying or receiving it classified it correctly. If the IRS decides that tuition remission for funded graduate students is taxable, then it’s pretty much taxable.

Also, as a side note to anyone here interested, because the tax code is so confusing and ambiguous, the IRS publishes a lot of interpretations and guidance documents (some of these documents end up having tremendous legal importance; I knew a lawyer who made literally tens of millions of dollars based on one). Publication 970 describes treatment of education expenses in a little more detail (https://www.irs.gov/publications/p970).

Thanks DC.

I’m still not seeing the argument that something called a scholarship that is dependent on your teaching automatically counts as a tuition reduction.

I’ll do a very philosopher thing and try to analyze the proposition expressed by 117(d) in predicate logic:

Here is the text again:

Except as provided in paragraph (2), subsections (a) and (d) shall not apply to that portion of any amount received which represents payment for teaching, research, or other services by the student required as a condition for receiving the qualified scholarship or qualified tuition reduction.

Some variables:

X – the money that is either the scholarship or the tuition reduction

P – the taxable payment for work done

W – the work done (research, TA, teaching)

So now we get:

If P is not of the kind mentioned in subsection (2), then

section (a) does not apply to P for any P such that

P is compensation for W and

W is a required condition for receiving X and

X is either a qualified scholarship or a qualified tuition reduction.

Lets assume that disjunctions in the tax code entail possible existential generalizations for both disjuncts (i.e. if the tax code says A is either F or G, then possibly there exists a tax situation in which A is F and possibly there exists a tax situation where A is G)

Together, this entails:

Possibly, some work W is a condition for receiving X and X is a qualified tuition scholarship.

Therefore, by 117(c) you getting tuition remission BECAUSE of your work as a TA or Researcher does not constitute a reason for this to count as an employee benefit tuition reduction.

I did read p970, p15, and p15b in all the relevant sections on scholarships vs. tuition reductions. Again, tuition reductions always show up in the context of Fringe Benefits. p970 has the most elaborate explanation of scholarships and tuition reductions.

I think the most relevant here is an example provided for what counts as a qualified scholarship:

Example 1.

You received a scholarship of $2,500. The scholarship wasn’t received under any of the exceptions mentioned above. As a condition for receiving the scholarship, you must serve as a part-time teaching assistant. Of the $2,500 scholarship, $1,000 represents payment for teaching. The provider of your scholarship gives you a Form W-2 showing $1,000 as income. Your qualified education expenses were at least $1,500. Assuming that all other conditions are met, $1,500 of your scholarship is tax free. The $1,000 you received for teaching is taxable.

Note: This is all within the explanation for 117(a-c)

p970 also gives the definitions of scholarship and fellowship that are used in the tax tool someone else mentioned:

A scholarship is generally an amount paid or allowed to, or for the benefit of, a student (whether an undergraduate or a graduate) at an educational institution to aid in the pursuit of his or her studies.

A fellowship grant is generally an amount paid for the benefit of an individual to aid in the pursuit of study or research.

I know at least my university specifically defines the taxable money I get as a fellowship, so it would be rather odd for the taxable portion to count as a fellowship. In a publication they released in regard to some reporting changes to accord with the affordable care act, they noted that fellowships and assistantships are quite different from wages for employees under the tax law (https://www.rochester.edu/provost/assets/PDFs/Taxation_of_GradStudentStipends_02032017.pdf).

Now, that is not to say that at some other Universities the relevant way to handle this is not by counting graduate students as employees with tuition benefits. I think Brian gives a relevant case below for the students at the law school, where, it seems, their tuition at law school is reduced for teaching classes in some other part of the University. That certainly looks like a case of 117(d). But the traditional graduate student stipend/fellowship/scholarship deal fits much better under 117(a-c).

I will suspend judgment on what this means for folks at other departments though, even though it seems fairly clear that the way the University of Rochester handles it does not fall under 117(d).

“I’m still not seeing the argument that something called a scholarship that is dependent on your teaching automatically counts as a tuition reduction.”

It doesn’t necessarily automatically count as one; you’re welcome to declare it as a non-qualified scholarship. But why do that?

Think of it this way; there are four different categories here:

1. Non-qualified scholarship (taxable)

2. Qualified scholarship (not taxable)

3. Non-qualified tuition reduction (taxable)

4. Qualified tuition reduction (not taxable)

It could be (1) if you really want, but why pay taxes when you don’t have to? It’s not (2), because scholarships are not qualified when there is a research/teaching component as per 117(c)(1). It’s not (3), because 117(d)(5) makes an exception for graduate students doing research and teaching, though again you can count it as tuition benefits if you really wanted to pay taxes on it.

So between (1), (3), and (4), you WANT it to be counted as (4) tuition reduction, because that is the only option among the three where you don’t pay taxes on it.

Where I did my PhD, the tuition remission was not taxed, but the salary provided by the stipend was. As per your example, look at your W-2 to see what’s declared as income. For me, it’s just the salary from the stipend. While it may be different for you, I find it really unlikely.

“It’s not (2), because scholarships are not qualified when there is a research/teaching component as per 117(c)(1). ”

Again, that’s not what 117(c) says. 117(c) excludes the compensation (P) for the work done required for getting the scholarship (X). Look again at example 1 from Publication 970 explaining that statute:

In the example you get a scholarship for $2500. In order to get it, you have to perform TA work. But the work is only compensated at $1000, so the remaining $1500 are part of your category (2), i.e. a qualified scholarship, so long as your tuition cost is at least $1500.

In more realistic numbers:

A philosophy PhD student gets a scholarship of $60.000. In order to get it, she has to do TA work. The TA work is worth $20.000, and the remaining $40.000 are covering the $40.000 in tuition. She only pays taxed on $20.000. That is the exact example from the tax publication you linked, and it is listed as an example under 117(c).

I’ll admit that if the institution somehow does not report/calculate something as a scholarship, then it might run afoul the lacking 117(d), but the argument that 117(c) excludes all scholarships that are dependent on TA or research duties is just a plain misreading of the law and the documentation.

That doesn’t mean the IRS or congress couldn’t issue some directive to change the interpretations, but given the law on the books, this is the right way to read 117(c).

Sorry for the double post, but I wanted to clarify from the IRS proposed publication for Title 26 1.117-6.

You can find the PDF here: https://www.gpo.gov/fdsys/pkg/FR-1988-06-09/pdf/FR-1988-06-09.pdf

And I got the pointer from here: https://surlysubgroup.com/2017/11/06/gop-raises-taxes-on-graduate-students-or-does-it/

That’s a blog post from A Notre Dame Law Professor specializing in tax law. Full disclosure: His latest tweet says that the bill will tax reductions (https://twitter.com/patrickw_thomas/status/928015776975654913) but he does so on the basis of unclear testimony cited from a Ways and Means staffer in a verge article (https://www.theverge.com/2017/11/7/16619246/tax-bill-trump-gop-cuts-and-jobs-act-graduate-students-tuition-waiver-reductions). What isn’t clarified in that exchange is the 117(a-c) vs 117(d) dispute though.

In any case, here is the text on how to determine which part of a scholarship and fellowship is payment for service. Note: If there is a procedure for determining it, then clearly there are cases in which some part of such is not payment for service.

(3)

Determination of amount of

scholarship or fellowship grant

representing payment for services.

If only a portion of a scholarship or

fellowship grant represents payment for

services, the grantor must determine the.

amount of the scholarship or fellowship

grant (including any reduction in tuition

or related expenses) to be allocated to

payment for services. Factors to be

taken into account in making this

allocation include, but are not limited to,

compensation paid by—

(i) The grantor for similar services

performed by students with

qualifications comparable to those of

the scholarship recipient, but who do

not receive scholarship or fellowship

grants;

(ii) The grantor for similar services

performed by full-time or part-time

employees of the grantor who are not

students; and

(iii) Educational organizations, other

than the grantor of the scholarship or

fellowship, for similar services

performed either by students or other

employees.

If the recipient includes in gross income

the amount allocated by the grantor to

payment for services and such amount

represents reasonable compensation for

those services, then any additional

amount of a scholarship or fellowship

grant received from the same grantor

that meets the requirements of

paragraph (b) of this section is

excludable from gross income. See

paragraph (d)(5), Examples (5) and (6) of

this section.

“given the law on the books, this is the right way to read 117(c).”

When the tax expert you’re reading is saying that this would tax graduate student tuition waivers, and the American Council of Education is saying that this would tax graduate student tuition waivers, and the spokesperson for the people who are writing the bill are saying that this would tax graduate student tuition waivers, I think we should consider the possibility that the bill would tax graduate student tution waivers, even if our untrained reading of the plain text gives some reason to think that it wouldn’t be taxed. It’s a “very philosophy thing” to assume we can read things like this outside of their actual content, but really, it’s not always appropriate. (And if you’re preparing reports for your fellow graduate students based on this, that seems to me to be a bad idea.)

If we want graduate students not to be taxed on their tuition waivers, we should urge our representatives not to pass a bill that doesn’t clarify that it doesn’t tax tuition waivers. There’s basically zero chance that thisb bill becomes law unchanged, so we have the opportunity to make ourselves heard, if we recognize the dangers. (As I understand it, in its current form the bill cannot be passed in the Senate under reconciliation rules, which means it would be filibustered by the Democrats.)

I have never heard of a university dicing up where your tuition reduction comes from (“So in addition to your $30,000 stipend, you also get a $50,000 tuition reduction, of which $20,000 comes from your teaching/research, while the other $30,000 is a no-strings-attached scholarship because you’re awesome”). If a university did to get around the removal of 117(d), the IRS would almost certainly disallow that kind of bookkeeping game, for the very reasons you quote: The IRS is not going to find that your stipend PLUS a significant portion of your tuition is worth that much, especially as tuition skyrockets. If it’s declared as a scholarship, under 117(c) they’ll figure out the fair market value of your services, and subtract it from the tuition and your stipend together. The resulting number will mean you are being taxed at a significantly higher rate. The example you cite stops holding true when you add “more realistic numbers.”

Kolja, I know argument from authority is a fallacy, but I’ll do it a little anyway: I literally paid for my masters litigating the tax code. A good chunk of my PhD dissertation dealt with issues of statutory interpretation. I am licensed to practice in 2 state and 3 federal jurisdictions. The language of the original statute was clearly written to try and capture taxes from employees given tuition reduction but carving out an exception for graduate students who receive tuition waivers as part of their funded graduate study.

And when it comes to analysis of the real-world implications of statutory language, you have to be less analytical and more continental. A lot of how it is interpreted and enforced is based on intent, meaning, common practice, etc. etc.. The guy you cite is being naive in my opinion when he suggests the GOP doesn’t know what they’re doing. They’re trying to get rid of the SALT deduction, which will hurt (at least in terms of numbers, if not intensity), far more people than the tuition reduction change. If passed as-is the Trump IRS will almost certainly consider your tuition benefits as largely taxable.

I also second Matt’s warning to be very careful what you are telling your fellow graduate students. Interpreting how laws (or proposed laws) will affect them is

(last part got cut off) practicing law without a license.

Thank you Matt and D.C. for that very helpful correction, and especially the warning of not accidentally giving legal advice. I also appreciate the patience in showing me how this argument from the current laws can be undermined by the intent of repealing 117(d) and subsequent interpretations of that intent. I did not remember the importance of that, and that is a good reason to think that even if the current language favors one reading, this consideration could overturn that. That helped me understand something I did not understand before: Why, in the face of the language of 117(c), an explicit “tuition scholarship” would now be taxed. In everything I had seen argued before, that was not clear to me, so I really appreciate you helping me see that. I’ll go with suspending judgment on what the IRS would do if this passed as is, noting that it largely depends on the Republican’s intent.

I’ll ask one more question on the interpretation of 117(c) though, D.C., leaving the intent of repealing 1179d) aside. The example I meant was the following dice-up: ” Congratulations on getting accepted. Because you’re so smart to get accepted to our PhD program, we’re giving you a full tuition scholarship. Just note: to keep the scholarship, you gotto do some TA gig. But don’t worry, we’ll compensate you with $20.000 a year to do that.” That sounds to me like a normal acceptance letter. Seeming result: $20.000 in taxable income. You do point out that the TA/teaching/lab duties could get valued at above the value of the fellowship, and then taxable income would eat into the tuition scholarship amount. That does sound like a real worry, and i believe you that the IRS could rule that the entire scholarship a tuition should be counted as a tuition remission instead by citing the intent of the repeal of 117(d). But apart from that, is the way I put it above a misreading of the law? I’m just trying to figure out where I might be misunderstand that part of it.

I also asked Patrick Thomas to clarify over twitter whether he thought the staffer cited in Verge understood the difference between 117(a-c) and 117(d), and he noted that

“I’m not 100% sure that they understand it. Regardless, my concern is that (1) it does seem to be their intent to repeal this exclusion, (2) universities who rely on section 117(d) may classify such waivers as taxable, and (3) if universities don’t, students may face IRS audits.”

and

“While I think my argument re: 117(a) is right, universities may not, and may withhold tax on students.” (https://twitter.com/patrickw_thomas/status/928635401769832448).

So he does think the first order evidence on the law on the books says one thing, but intention and interpretation can change what it in fact comes to.

In terms of your advice, Matt, to take action. Given that commenting to Democrats isn’t much help, I did contact the Republican contender for my local house seat that has some non-zero chance of winning elections and asked him for clarification. While he can’t vote in congress, he might still have some impact, and I happen to have met him a few times in his current function as town supervisor. That’s about the best I can do on that end, given where I’m a resident.

Now, here is a meta question (In my more experienced role qua epistemologist):

I appreciate the call to defer to experts, and I especially appreciate the warning on not giving legal advice. However, something strikes me as a bit irksome about that. Given that we’re, of sorts, discussing the repercussions of political activities, specifically the passing of laws, my understanding was that citizen (or alien resident) discussion and debate was a good thing. We do this in broad general terms all the time without looking at the details.

What happened to me is that I was perfectly fine and accepted the report in the news on the tax impact. I even I posted it on my own facebook wall condemning the move. But then I came across the argument here that said: “Wait, this is a misreading of the tax code. Here is what it actually says in detail…” I was incredulous, but really wanted to know, and given that I only had higher order testimony and was presented with some coherent first order defeater, I didn’t know what else to do but look at this in detail myself. Notably, no one had made an in depth argument addressing the “tuition scholarships” from 117 (a-c). Now, it might be the case that looking at the tax code myself was a grave mistake I should not have made. Maybe getting more evidence was the wrong thing to do, epistemically.

Notably, I didn’t start looking at the tax code until someone else, a putative expert, suggested that the first order evidence did not support the claims in the news articles. When I did look at it, that argument seemed plausible. Moreover, it seemed that lots of people misread the language in 117(c) to mean “Any scholarship conditional on services rendered is taxable” which is not what it says. So now I had someone suggesting the first order evidence pointed one way, my own looking into it coming to the same conclusion, and a number of disagreeing higher order testimony.

From this we get an important question in the epistemology of disagreement:

What if you know of some expert disagreement, you look at the first order evidence as a novice, come to agree with the minority and understand the argument by the minority, and you do not know or understand the argument from the first order evidence of the other side. Moreover, you have some error theory, on what you think the evidence points to, why the experts on the other side might get this wrong (along with some explanation from political motivation). And finally, you don’t have any way of accessing the argument from the other side.

What should you believe in that scenario? What should you do?

Is the advice something like never trust yourself when faced with majority expert disagreements when you don’t know the argument from the other side?

What if you know the detailed argument from neither side? Usually when we’re arguing about politics or the implications of some proposed law on society we engage in political debate without knowing the exact legal arguments from either side. So, is it somehow worse to try to look at the legal arguments in detail? That also seems odd. I don’t think having less evidence in a political dispute is better than having more. know few people criticizing the plan to decrease corporate tax form 35% to 20% that have engaged with commentary from both liberal and conservative economists, even though they’re hashing out disagreements on the exact impact in the journals and on their blogs. Would it be bad to look at the detailed models some on either side propose in making their arguments as an economics novice? Especially when faced with the need to take political action, looking at the details could be good, even if one gets it wrong. But maybe one should never do that.

A further note on the legal advice jeopardy: If I get an email from the GSR saying “Your taxes will go up. See this article.” And I sent an email back “Someone says they won’t. Here is an explanation of the argument they make from the tax code.” Here is where the analytic philosopher side of me wants to complain about the criteria of what counts as legal advice. Both apply a particular law (proposal) to a particular circumstance. One does so on the basis of a news articles. One does by re-stating an argument from a social media website in a cleaned up version. Especially since the real question is “What would happen if this bill passed?” that seems to come close to barring individuals from discussing the political implication of some proposed law if they get too close to the evidence that matters, i.e. the changes in the legal code. That just seems undemocratic, but I get the dangers, especially if emails are phrased in the “here is what the law is” kind of way. At the time, I really just meant well because if the proposal indeed does not have the implications, and if we could know that, then people would be getting stressed and worried unnecessarily.

Finally, there is the question of the GOP intention. As you both point out, that matters for interpreting the law, and you assume the intention is to cut all grad tuition scholarships/remissions. I had wanted to approach this in exactly the opposite direction. My assumption was that we could deduce the GOP intention by looking at what the resulting law would and would not count as taxable income. And the more I looked at the details it seemed that the intention of 117(d) was intended to cover employee benefits and 117(a-c) was intended to cover tuition scholarships for students, so I thought that was a good guide towards coming to a conclusion about the GOP intention.

Part of what fueled that incredulity was that repealing the scholarships would constitute the largest tax hike on anyone affected by this tax bill with the possible exception of people that have medical expenses in proportion to their income that matches the proportion of tuition scholarships/remission to take home pay ration of grad students. Going from $20.000 to $70.000 in taxable income is a tax increase I have never heard of, and everything else that people are discussing on the tax plan is peanuts in comparison (with the exception of high medical expenses), relative to an individual.

So now I realize how much intent matters. I had hoped to deduce intent by finding out about the tax implications of the remaining laws, but that seems to have been going at it completely backwards. I’m still, I’m wondering why they’re not repealing 117 all-together in that case. If no grad student can ever get a scholarship tax free, why not go all the way and make undergrads pay taxes for them as well? Maybe that’s too much political backlash, although they did cut student loan interest deductions.

Thanks again for the really helpful comments and bearing with me on that. I feel like I learned a lot, and I’m eagerly awaiting someone to authoritatively declare the intent behind the law while doing what I can that it won’t affect the tuition remissions and scholarships.

“But apart from that, is the way I put it above a misreading of the law? I’m just trying to figure out where I might be misunderstand that part of it.”

I don’t think you’re misunderstanding something exactly; the text is ambiguous, and your analysis is one valid interpretation when looking at it linguistically. But when you take the context of how funding is handled traditionally in the university system for funded graduate students, and the price of tuition now, it seems to me and I guess a lot of the other commentators, that traditional tuition remission is tuition reduction, not a scholarship.

Legal pragmatism — particularly its focus on contextual and instrumental precepts of that philosophy — seems to me the best analytical approach to this and other sections of the tax code. The code is so massive, ambiguous, and complex largely because it tries to preemptively address attempts to render taxable income non-taxable. Partly because of this the IRS has a lot of leeway to try and interpret the rules; first through formal and informal rulemaking, then through general guidance and circulars, THEN through individual responses to individuals and entities that request clarification of a point. And even then, there’s plenty of litigation, and different courts will interpret different provisions differently. Ultimately, though, If the IRS thinks Congress wanted to hit graduate students, then the IRS will almost certainly try to hit graduate students.

If something like this went through, I suspect universities would negotiate with the IRS to try and figure out an acceptable way to define ivvy up scholarships so you don’t have a lot of grad student audits, but I suspect that whatever the negotiation ends in will mean significant additional taxation for the students.

There’s nothing wrong with a non-expert agreeing with a minority opinion, even a very unpopular minority position, over a point of law. There is no real right or wrong answer, because at the end of the day it’s people making judgment as to how laws are interpreted or enforced. For all we know, your interpretation might ultimately be considered the correct one, but like a lot of real-world things we’re playing a game of probabilities. Law is what the courts make it, and who knows what they (or the IRS) will determine what’s right, though if they think Congress has a certain intent they are far more likely to interpret the law with that intent in mind.

I would suspect they’re not repealing 117 in its entirety because it would just bring too much political heat, even among the Republican base. Telling a Trump booster in Alabama that they’re going to be taxing all those effete elitist intellectuals in graduate school might receive a standing ovation, while telling him they’ll also make it a lot harder for the Crimson Tide to recruit scholarship football players might be something else.

As for the legal advice thing, law is a big, very protective guild, very jealous of their prerogatives. There’s a blurry line determining what counts as legal advice, but generally it generally arises when you’re interpreting the law for a specific set of facts for an individual or limited number of people. The way even lawyers on blogs plaster “this is not legal advice” all over is because the state bars actually suggest you do that, otherwise you can run into trouble. And again, you run into the same problem with the IRS above — it comes down to how the relevant authorities will interpret it.

Thanks for the gracious response, Kolja. D.C. has said everything I might about the practical aspect (and more, since D.C. speaks from expertise and I don’t).

About the epistemological aspect, I guess again I’ll agree with D.C. that there’s nothing wrong with siding with a minority expert view–but for law in particular the way law gets interpreted can get very far away from the kind of logical analysis we’re inclined toward. This came up a lot in the litigation over the Affordable Care Act, where one of the lawsuits involved a question of whether, as written, a definition in one part of the law strictly speaking implied that health-care subsidies couldn’t be paid in states that used healthcare.gov exchanges rather than setting up their own exchanges. And the Supreme Court eventually decided–as I roughly understand it–that that couldn’t be the proper interpretation because it would lead to a ridiculous outcome contrary to the intent of the bill. (Also there’s the question of Chevron deference to the ruling of the administrative agency, which didn’t come up, but gets discussed there.)

And as D.C. says what we’re ultimately concerned about is the way the law actually gets applied, which is a question of how the relevant authorities would decide to apply it. So that ultimately we can’t be quite sure whether the majority or minority expert opinion will prevail–but what we can conclude is that this might lead to tuition waivers being taxed, which given the disastrous effect is something to be concerned about.

(And good on you for contacting the local Republican potential candidate! If the actual congressfolk hear from their candidates that the issue is hurting them, it might have an impact, and upstate NY Republicans are some of the key votes on this bill because many of them are unhappy about what it would do to their constituents, specifically with repealing the state and local tax deduction bill. My representatives and senators are so safely Democratic, or Democratic-caucusing independent, that I don’t have much leverage there–they’ll oppose this bill no matter what.)

I think the references to ‘child’ here are confusing things. As you say, 117d covers fringe benefits *to employees* as well as to children of employees.

At least some people who serve as GSIs get tuition reductions as part of their own teaching. That’s certainly true in Michigan philosophy for graduate students from other programs; law students love teaching for us for just this reason.

The worry is that, at least in terms where the PhD student is teaching, and so the PhD student is both a student and an employee, the tuition reduction will be treated as being part of their employment relationship, not part of their student relationship.

This could work out not being a problem, but I really don’t think that there is only one way to read 117 after d is repealed. The way it would then be written is (to this non-lawyer) confusing in the case where the waiver recipient is both a student and an employee.

Another aspect of this is that it would (and most likely is intended to) make tuition remissions given to employees’ dependents taxable, as C observed above. I didn’t belabor this before, because though it has the potential to affect me, there’s a much better argument for my getting taxed on any tuition benefits I might use than on graduate students getting taxed on their tuition waivers. But (as C also pointed out) the effects could be devastating on less highly compensated staff members counting on tuition waivers to send their kids to college.

More on this here from Daniel Marans and in this twitter thread from Len Burman, who points out the unfairness of imposing a tax burden now on an employee who may have worked for years with the promise that their children would have their college educations paid for. Burman argues that if these benefits are to be taxed, they should be taxed when earned as opposed to in a lump sum when paid out (though as he observes there would be a lot of problems implementing this). I don’t know how this accords with other taxable benefits.