Unscientific Poll Results: Nearly 40% Of Respondents Take Out Loans To Get PhD In Philosophy

A couple of weeks ago I set up a poll asking about whether philosophy graduate students took out student loans while in their PhD programs. This is, of course, not a scientifically sound way of getting at the actual numbers, as the respondents are self-selecting and there is no way to tell if they are at all representative of the broader population.

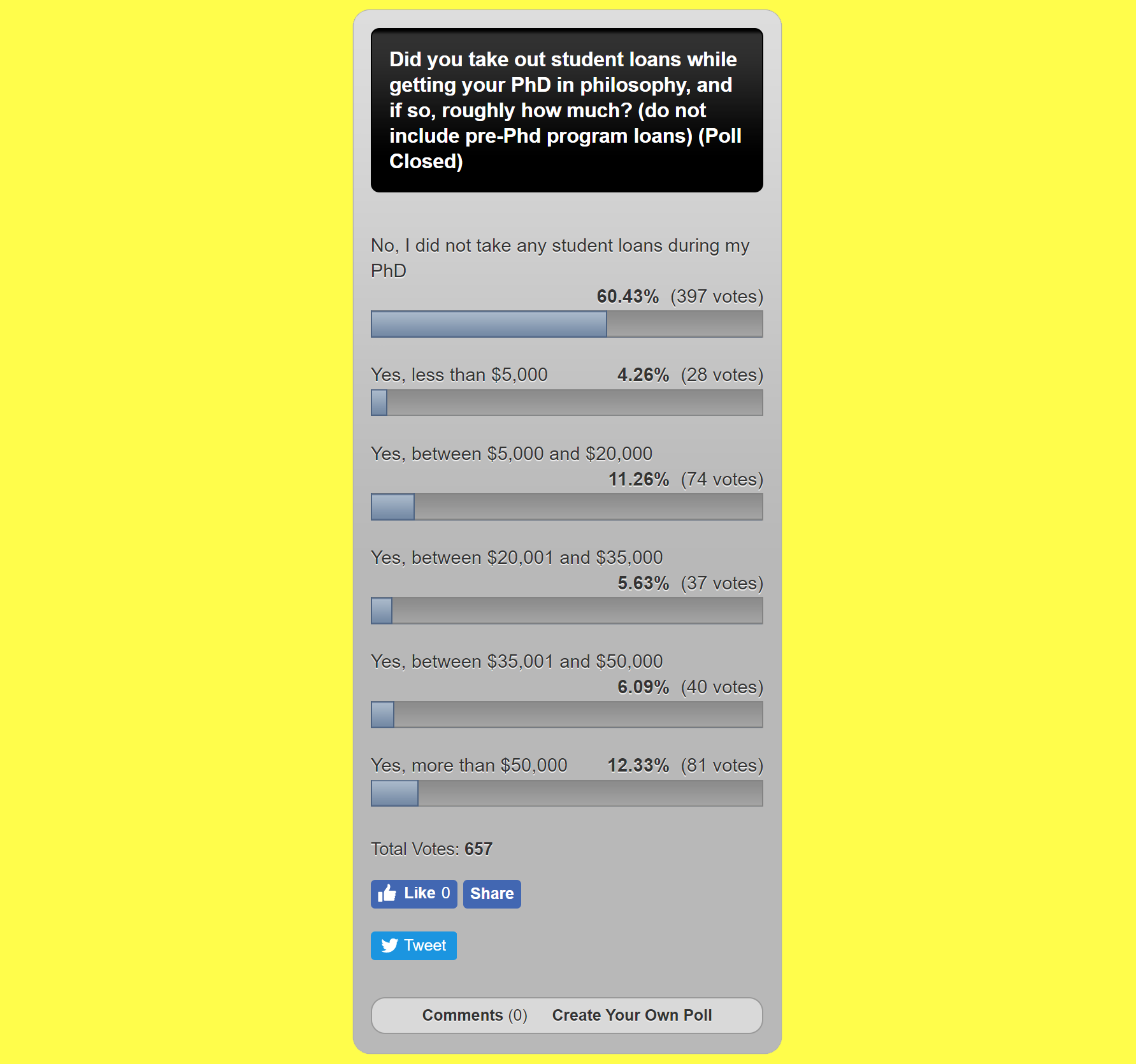

During the several days the poll was open, there were 657 respondents, and of them, nearly 40% said that they took out a student loan while getting their PhD in philosophy, and nearly 25% borrowing over $20,000.

Here are the full results:

Note that respondents were only asked about student loan programs, not consumer debt (e.g., car loans, credit cards, etc.).

Such numbers, were they the products of a more sound inquiry, might suggest looking at various ways philosophy departments or universities might assist students (either through opportunities for further aid, summer work, financial counseling, restructuring of the graduate school schedule to allow outside employment, etc.).

Perhaps, though the numbers are sufficient to prompt a more rigorous attempt to collect data on student debt among philosophy PhD students.

Other than, you know, actually paying/funding us more, I think that making financial counselling easily available is a great idea. It doesn’t come easily to everyone and you can easily get in over your head if you’re not careful.

It would be interesting and perhaps useful to know how many people who borrowed money had some measure of funding that nonetheless proved insufficient, and how many attended entirely unfunded programs, such as in the UK, where it seems funding is much harder to come by.

I would also be curious about the possible correlation between those who must borrow for their undergraduate degrees, and those who acquire debt in a PhD program.

When I went through grad school, nobody warned us about how dire the job situation was (it is worse now). I ended up with a tenure-track position and ultimately it got tenure, but not everyone I knew was so lucky, and after devoting their lives and money to philosophy for years, were left in debt and wondering what to do with their lives. I think it is unethical not to warn prospective grad students about just how hard things are.

Hey Nonny Mouse: I entirely agree! And Justin: kudos for running this (admittedly unscientific) poll. I think it is vital for prospective grad students to not only be made aware of grad-program attrition and placement-rates (and the sorry state of the job-market), but also of just how many of us finish our PhDs in debt. I finished my BA with zero debt but racked up $50K by the time I finished my PhD…which I will finally finish paying off next year. When I was floundering on the academic market (for a number of years), the debt I had incurred was a massive financial weight on me and family, as well as a source of great daily anxiety. I’ve heard so many people say, “Don’t go into debt to get a philosophy PhD.” Maybe so…but it’s easier said than done.

I entered grad school in 1976–and even then I was aware that job offerings in philosophy were on the decline. I want to say that I was aware of an APA declaration about that in those years, but I have no proof of that. Anyway, even way back then our cadre of grad students knew of the risks of unemployment, and they were substantial. But thanks to one successful interview out of 70+ apps in 1980-81–the only interview I’ve ever had–I was able to pay off my (rather relatively meager) debt. Maybe I should write a sequel to Neil Levy’s excellent Hard Luck–about my own Dumb Luck. I wish grads these days some version of that.

This is about the time I entered grad school (1970 for me). Got my MA in ’73 and entered PhD program. At the time I did the APA did send warnings about limited opportunities and my grad school confirmed that. I persisted with a grant and some aid, but no loan. Mostly my wife and I worked to pay tuition (which was, of course lower than now, but not cheap by 1970 standards), and it took me many years to finish the PhD as we could only pay for fewer than full load. Spent career teaching philosophy, 12 years as an adjunct professor, the rest as tenured eventually full professor. I decry how hard this would be today, given the costs and fewer jobs. I applaud all who are struggling now and hope you all can keep it up and be rewarded with a satisfying, full-time job.

Wow. If anyone does gather more data on this, I’d also be curious to know how many entered Ph.D. programs planning to take out loans vs. how many found themselves in a bind later once there were already a lot of sunk costs (e.g., if finishing turned out to take longer and they ran out of funding).

In my department, we run a bi-annual survey of our graduate students and among the questions we ask are a few about student loans, both grad school loans and existing debt load (whether from undergrad or grad). I think doing this has been valuable in a couple of ways: keeping us apprised of the facts of our students’ lives and giving us data we can carry to administration when asking for better funding. More generally, I think it increases faculty sensitivity to the lives of the graduate students to have such information, making us less likely to be cavalier about expecting grad students to undertake activities, travel, etc., that will cost them financially. Even when there’s not much we can do, it seems good to know where the students are coming from and what they’re carrying.

As a STEM PhD grad, I really do not understand this. It was made very clear to me by my undergrad faculty “If you don’t get full funding for your PhD from an institution, you don’t go.” Given the the weakness of the job market in most academic fields, it seems unconscionable to not warn students against pursuing degrees that not only have weak job prospects but will also foist additional financial burdens upon them.

That’s pretty standard advice in philosophy as well. But just because you have “full funding” doesn’t mean that you won’t find some reason to take out student loans. Two issues that come to mind off the top of my head are that some students might have family issues that require more money (a child, or medical or personal care issues for a partner or parent), and that often a “fully funded” program covers 5 or 6 years and a person sometimes requires an extra year or two to finish up. On top of this, the level of stipend and cost of living at various PhD programs can vary greatly, so there may be particular programs that pay almost enough to live in their city, but students regularly use savings or loans to cover the rest.